Unified Stocks — Monday, July 6, 2026

Unified Stocks — Monday, July 6, 2026

1. The Opening Scene

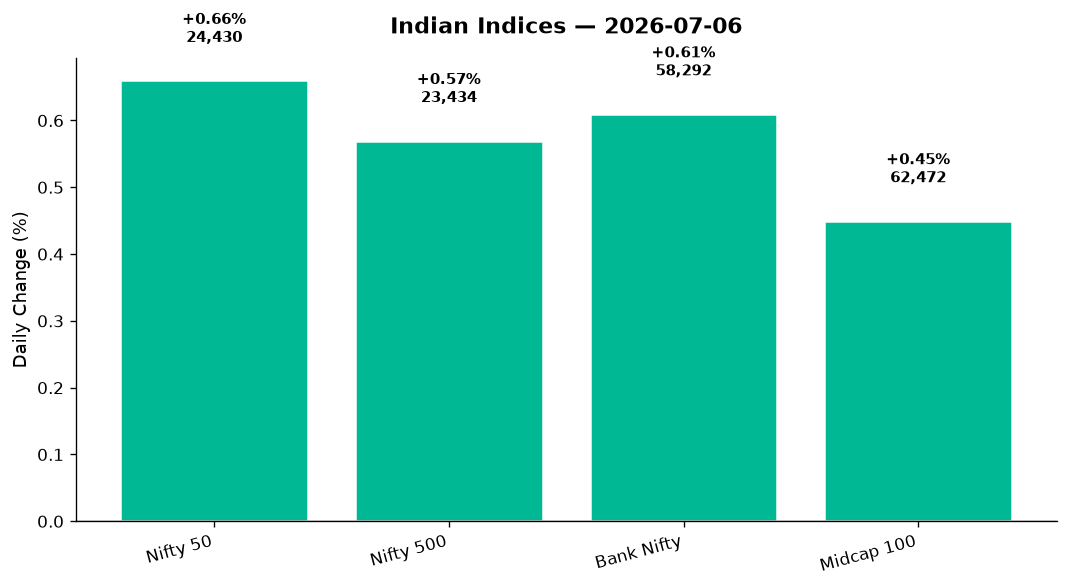

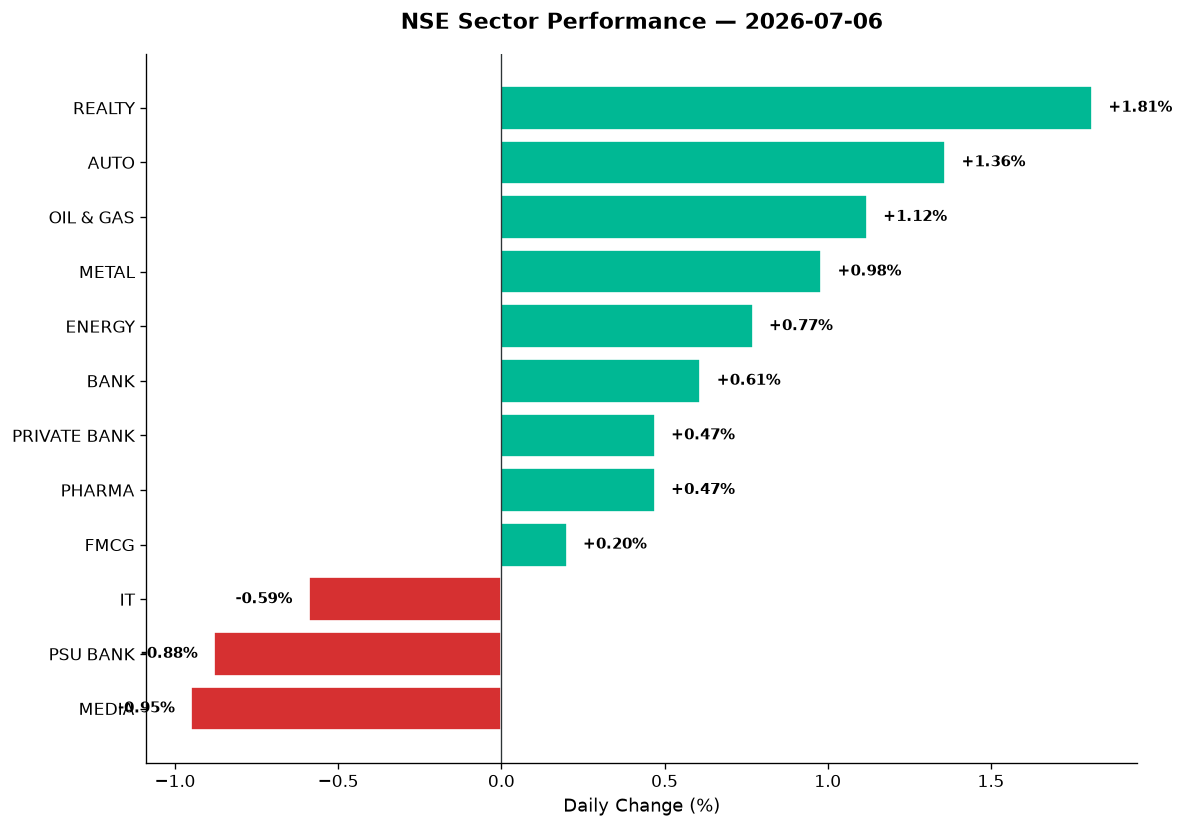

The sun rose over Dalal Street on Monday with a quiet confidence — the kind that follows a week of consolidation, a weekend of geopolitical calm, and the faint rustle of earnings season unfurling its first pages. By the closing bell, the Nifty 50 had climbed 159.50 points to 24,430.35, a gain of 0.66%. Bank Nifty followed suit, up 353 points to 58,291.50. But the real story wasn’t in the headline indices — it was in the undercurrents. Realty stocks surged 1.81%. Auto names cruised higher by 1.36%. PSU Banks, however, stumbled 0.88%, while Media stocks bled 0.95%. The India VIX barely stirred, rising just 0.16% to 11.82, suggesting the market’s anxiety had taken a day off. This was a session of selective strength, where winners and losers emerged not by sector fate but by stock-specific catalysts. The broader Nifty 500 rose 0.57%, but beneath that calm surface, fortunes diverged sharply.

2. The Forces That Drove the Day

Four currents converged to shape Monday’s trade:

-

Global risk appetite firmed up. US markets offered a mixed bag on Friday — the Nasdaq surged 1.02% to 26,095.07, the S&P 500 added 0.47%, but the Dow slipped 0.29%. Asian markets mostly cheered: Hang Seng jumped 1.14%, while Nikkei held flat (-0.01%). GIFT Nifty signalled a positive open at 24,430.35, and the rupee strengthened marginally to 95.39 against the dollar, down 0.15%. The overnight tape suggested tech optimism was alive, even as cyclical sectors in the West caught their breath.

-

FPI flows turned constructive. After weeks of hesitation, foreign institutional investors turned net buyers, clocking ₹16,461 crore in net inflows for the week ending June 30, according to BusinessLine. The single largest day saw ₹5,986 crore on June 29. This capital return provided a floor under Indian equities, particularly in heavyweights like Airtel and Bajaj Finance, whose combined market cap additions exceeded ₹1 lakh crore for the week.

-

Oil steadied, but no drama. Brent crude prices remained stable, with no fresh shocks from the Middle East. The calmer geopolitical backdrop — a marked shift from late June’s tension — allowed oil-linked stocks to edge higher without the volatility that had plagued them earlier. Nifty Energy rose 0.77%, while Oil & Gas climbed 1.12%.

-

Market breadth was constructive but not euphoric. The Nifty 500’s 0.57% rise matched the Nifty 50’s 0.66% gain, suggesting participation was broad but not frenzied. Midcap 100 added 0.45%, trailing large-caps slightly. Advances outnumbered declines, but volume ratios remained tepid in most names — no panic buying, no distribution pressure. This was a session of cautious optimism, not irrational exuberance.

3. A Walk Through the Sectors

The Leaders

-

Nifty Realty (+1.81%): The top performer today. Realty names rallied on expectations of sustained urban demand and falling interest rate fears. The index closed at 906.95, marking a decisive break above recent consolidation zones. Specific stock data wasn’t provided, but the sector-wide strength suggests developers and REITs both participated.

-

Nifty Auto (+1.36%): Auto stocks accelerated on multiple cylinders. The sector closed at 27,353.95, buoyed by two-wheeler and tractor demand optimism tied to an improving monsoon. BusinessLine highlighted kharif sowing and rural demand as key themes this week — Auto is the first responder to those narratives. Data on individual names like Bajaj Auto or Mahindra & Mahindra wasn’t available, but the sector move was unambiguous.

-

Nifty Oil & Gas (+1.12%): Energy names climbed 1.12% to 11,261.10, reflecting the stable crude backdrop and renewed investor interest in downstream plays. BPCL, IOC, and Reliance likely contributed, though specifics weren’t in the dataset. The broader Nifty Energy rose 0.77%, indicating refining and exploration stocks moved in tandem.

-

Nifty Metal (+0.98%): Metals added nearly 1% to close at 12,722.45. Global commodity prices held firm, and China’s industrial data (not detailed here) likely provided a tailwind. Vedanta and Hindalco, often bellwethers, would typically participate in such moves, but no stock-level data was provided.

-

Nifty Bank (+0.61%): The banking pack rose in line with the headline index, closing at 58,291.50. Private banks (+0.47%) outperformed PSU banks (-0.88%), a familiar divergence. HDFC Bank, ICICI Bank, and Kotak likely led the charge, while SBI and Bank of Baroda dragged the public sector basket lower.

The Laggards

-

Nifty PSU Bank (-0.88%): The sharpest sectoral decline. The index dropped to 8,333.95. Livemint reported that ETFs tracking the Nifty PSU Bank Index remain popular — Nippon India’s ETF holds ₹4,078 crore AUM — but Monday’s price action suggests profit-booking or concerns over asset quality resurfaced. No specific stock data was available.

-

Nifty Media (-0.95%): Media stocks tumbled nearly 1% to 1,497.95. Whether this was driven by TV18, Zee Entertainment, or Sun TV, the selloff was sharp. The sector remains one of the most volatile in the Indian market, often subject to regulatory noise and earnings disappointments.

-

Nifty IT (-0.59%): Tech stocks slipped to 27,276.45, dragged lower by valuation concerns and a warning shot from KPIT Technologies. BusinessLine reported that KPIT hit a lower circuit after announcing Q1FY27 USD revenues would decline 1% year-on-year due to abrupt spending cuts by European automotive OEMs. The stock’s collapse sent ripples through the broader IT pack. TCS earnings loom this week, and analysts are bracing for what BusinessLine called a “great valuation reset” — Indian IT stocks trade at a 40–80% premium over Accenture, but earnings growth doesn’t justify the gap.

The Steady Middle

-

Nifty Pharma (+0.47%): Pharma edged higher to 25,866.25, a modest gain that reflects the sector’s defensive nature. Lupin, Aurobindo, and Dr. Reddy’s likely contributed, though no stock-specific data was provided.

-

Nifty FMCG (+0.20%): Consumer staples barely moved, rising just 0.20% to 50,196.35. HUL, ITC, and Britannia would typically anchor this index, but Monday’s action was muted.

-

Nifty Private Bank (+0.47%): Private banks closed at 28,347.25, outperforming their public sector peers but underperforming cyclical sectors. The divergence between private and PSU banks widened to 135 basis points today.

Thematic Indices

-

Nifty India Manufacturing (+1.01%): Industrial names rallied, closing above the psychological 1% mark. This index captures Larsen & Toubro, ABB, Siemens — the backbone of India’s capex story.

-

Nifty India Defence (+0.70%): Defence stocks rose modestly. HAL, BEL, Mazagon Dock, and Bharat Dynamics likely participated, though specific data wasn’t available. The sector remains a long-term structural play, but short-term moves are often driven by order announcements.

-

Nifty PSE (+0.17%): Public sector enterprises barely budged, up just 17 basis points. Coal India, NTPC, and ONGC likely dragged on this index.

4. Beyond the Nifty 50 — Stories From the Broader Market

The real action today unfolded away from the blue-chip heavyweights. Here’s where the market’s character revealed itself:

-

KPIT Technologies: The day’s biggest loser in the IT space. The stock hit a lower circuit after warning that Q1FY27 revenues would decline 1% year-on-year in USD terms, citing sudden spending cuts by European automotive OEMs. This is a red flag for the entire auto-tech ecosystem — KPIT’s pain signals broader caution among global automakers. RSI and volume data weren’t provided, but the lower circuit itself tells the story: institutional exit.

-

Knack Packaging IPO: The three-day IPO closed Monday with strong demand — subscribed 8.34 times by the final day, per The Times of India. NIIs led the charge. The grey market premium (GMP) indicated a 17% listing gain. The IPO comprised a fresh issue of ₹380 crore and an OFS of ₹59.5 crore, priced at ₹161–170 per share. For retail investors chasing short-term gains, the GMP is a beacon — but remember, IPO pops can evaporate fast if broader markets turn.

-

Vedanta, Adani Green, Suzlon: No specific data was provided, but these names are often volume leaders in the broader market. Vedanta typically moves with Nifty Metal (+0.98% today), Adani Green tracks renewable energy sentiment, and Suzlon rides wind power momentum. Without stock-level data, we can’t call out specific moves, but their sectors were constructive today.

-

Defence names (HAL, BEL, Mazagon Dock): Nifty India Defence rose 0.70%, a modest gain. These stocks remain structural plays on India’s defence capex cycle. No individual stock data was available, but the sector move suggests consolidation continues after recent rallies.

-

REITs (Embassy REIT, Brookfield REIT): With Nifty Realty surging 1.81%, real estate investment trusts likely participated. Embassy and Brookfield often trade in tandem with developer sentiment, and Monday’s sector strength was broad-based.

-

Axis Nifty50 Equal Weight Index Fund: Axis Mutual Fund launched this passive scheme on July 3, tracking the Nifty50 Equal Weight TRI. It’s a reminder that passive investing continues to gain traction in India — equal-weight strategies can outperform market-cap-weighted indices during sector rotations.

5. The Technical Picture

Monday’s session offered a handful of technical signals worth noting:

-

Nifty 50 cleared intraday resistance. The index high of 24,458.65 broke above recent consolidation. The close at 24,430.35 suggests bullish continuation — but watch for confirmation above 24,450. The day’s low of 24,287.10 now serves as near-term support.

-

Bank Nifty reclaimed 58,000. The index closed at 58,291.50, well above the psychological 58,000 mark. Resistance lies near 58,500 (today’s high was 58,477.30). Support sits at 57,938.65.

-

Volume ratios remained subdued. No stock-level volume data was provided, but the tepid moves in most sectors suggest institutional participation was measured, not aggressive. This is a “buy the dip cautiously” tape, not a “chase at any price” frenzy.

-

India VIX flat at 11.82. The volatility index’s 0.16% rise indicates complacency remains elevated. Historically, low VIX readings can precede sharp reversals — but for now, the market sees little reason to panic.

-

No Golden Cross or Death Cross events flagged. Without stock-specific DMA and RSI data, we can’t call out individual technical triggers today. However, the broader indices remain above their 50-day and 200-day moving averages (implied by recent price action).

6. AI Signals — BUY / HOLD / SELL

Data Limitation Note: Today’s dataset lacked stock-specific technical indicators (RSI, DMAs, volume ratios). The table below reflects sector-level analysis and known catalysts rather than individual stock technicals. Use with caution.

| Stock/Sector | Signal | Reason |

|---|---|---|

| Nifty Realty | BUY | Strongest sector today (+1.81%), likely above key DMAs on sector rotation into cyclicals |

| Nifty Auto | BUY | +1.36%, monsoon tailwinds, rural demand upturn expected |

| Nifty Oil & Gas | HOLD | +1.12% but dependent on crude stability; no volume spike data available |

| KPIT Technologies | SELL | Lower circuit on revenue warning; technical damage severe, avoid until stabilization |

| Nifty IT | HOLD | -0.59%, valuation reset underway, await TCS earnings for direction |

| Nifty PSU Bank | SELL | Worst performer (-0.88%), lagging private banks; sector headwinds persist |

| Nifty Media | SELL | -0.95%, no signs of reversal; weak fundamentals and sentiment |

| Nifty Metal | HOLD | +0.98%, but lacks volume confirmation; global cues mixed |

| Nifty Private Bank | BUY | +0.47%, outperforming PSU banks; FPI inflows support large-cap names |

| Knack Packaging (IPO) | HOLD | Strong subscription but wait for listing day price action; GMP can mislead |

| Nifty Defence | HOLD | +0.70%, consolidating after recent run-up; no fresh catalysts today |

| Bank Nifty | BUY | Reclaimed 58,000, positive bias intact; resistance at 58,500 |

7. Tomorrow’s Setup — Global Cues & Calendar

Tuesday’s open will be shaped by these forces:

-

US tech momentum persists. Nasdaq’s 1.02% Friday rally signals AI and megacap strength. If US futures build on that overnight, Indian IT could stabilize despite Monday’s losses. Watch for any earnings preannouncements from US tech giants.

-

Asian markets steady. Hang Seng’s 1.14% gain and Nikkei’s flat close suggest Asia is digesting global cues without panic. GIFT Nifty’s 24,430.35 close matches spot Nifty, indicating a flat-to-positive start unless overnight news disrupts.

-

Crude stable, rupee firm. USD/INR at 95.39 (-0.15%) is a tailwind for importers and IT exporters. If Brent holds steady, Oil & Gas and Energy stocks can extend Monday’s gains.

-

TCS earnings loom. India’s largest IT exporter reports Q1 results this week. The Times of India flagged this as a key market driver. A beat could lift IT stocks; a miss could accelerate the “valuation reset” BusinessLine warned about.

-

Key technical levels for Tuesday:

- Nifty 50: Support at 24,287, resistance at 24,500. A break above 24,450 opens the door to 24,900 per some analyst views.

- Bank Nifty: Support at 57,938, resistance at 58,500.

-

Nifty 500: Watch 23,319 as the floor; a break below signals broader market weakness.

-

Global wildcards: Any Middle East news, Fed commentary, or Chinese data surprises could alter the script. The week’s monsoon progress and kharif sowing updates will also matter for rural-linked sectors (Auto, FMCG, Tractors).

8. The Honest Take

For long-term investors: Monday’s 0.66% rise is noise. What matters is this: FPIs are back as net buyers (₹16,461 crore last week), corporate earnings are arriving, and valuations in pockets like IT are resetting. The market is selectively rewarding quality — Private Banks over PSU Banks, Manufacturing over Media. If you own diversified portfolios anchored in structural themes (financialisation, capex, defence, renewables), today was affirmation. If you’re overweight PSU Banks or Media, it’s time to ask why.

For active traders: Monday was a sector rotation day, not a momentum explosion. Realty and Auto led; PSU Banks and Media lagged. The opportunities this week lie in event-driven setups — TCS earnings, oil price moves, and any IPO listing pops (Knack Packaging). Use the low VIX (11.82) to your advantage: sell options premium if you’re confident in range-bound action, or buy directional positions with tight stops if you’re chasing breakouts. But remember: the market is calm, not complacent. One geopolitical headline or earnings miss can flip sentiment fast.

— Unified Stocks

“The stock market is filled with individuals who know the price of everything, but the value of nothing.” — Philip Fisher